3D Secure Payment Gateway: How OTP Transactions Work

Table of Content

Download Paymattic – it’s Free!

Subscribe To Get

WordPress Guides, Tips, and Tutorials

We will never spam you. We will only send you product updates and tips.

Every time a customer hesitates at checkout because they’re not sure their card details are safe, you’re losing a sale.

That hesitation is exactly what a 3D Secure payment gateway is built to fix.

According to Visa, authenticated transactions show close to a 45% reduction in fraud compared to non-authenticated ones. That’s not a small number when you’re running an online store or accepting recurring payments.

So in this article, we’ll break down what a 3D Secure payment gateway actually is, how it works step by step, and how it’s different from a 2D payment gateway.

We’ll also walk you through setting up a 3DS payment gateway on your WordPress site.

Key Takeaways

- A 3D Secure payment gateway adds an OTP or biometric verification step to confirm the cardholder’s identity before a transaction is approved.

- The “3D” refers to three domains involved in verification: the acquirer, the issuer, and the interoperability domain (the card network).

- 3D Secure 2.0 replaced the older, clunkier OTP-only flow with risk-based authentication, approving most low-risk transactions frictionlessly.

- Authenticated transactions see up to a 45% reduction in fraud and a 9% lift in authorization approval rates, per Visa.

- 3D Secure generally shifts chargeback liability from the merchant to the card issuer, protecting your revenue and reducing dispute workload.

- 2D payment gateways are faster since they skip OTP verification, while 3D Secure gateways trade a bit of speed for stronger fraud protection.

- Paymattic supports most major 3D Secure payment gateways, including Stripe, Razorpay, Mollie, Flutterwave, and Xendit, with no coding needed to set up.

What is 3D payment gateway?

A 3D Secure payment gateway is a payment authentication system that adds an extra verification step (OTP) to online credit and debit card transactions. Instead of just checking the card number, expiry date, and CVV, it confirms that the person entering those details is actually the legitimate cardholder.

The key differentiator here is the OTP, or one-time password. Once a customer enters their card details, most 3D Secure payment systems send a one-time code to their phone or email that they need to enter before the payment goes through.

That single extra step is what separates a 3D Secure payment gateway from a standard checkout. A 2D payment gateway skips this OTP step entirely and completes the transaction using just the card details.

The “3D” stands for three domains, which are the three parties involved in verifying the transaction:

- Acquirer domain: The merchant and their bank

- Issuer domain: The bank that issued the customer’s card

- Interoperability domain: The card network handling the exchange, like Visa or Mastercard

You’ve probably seen 3D Secure payment protocols in action without realizing it.

Visa’s Verified by Visa, Mastercard’s SecureCode, and American Express SafeKey are all examples of the same underlying 3D Secure payment gateway, just branded differently by each card network.

In every case, the OTP (or a biometric equivalent in newer versions) confirms that the person paying is who they say they are.

We’ll get into the full 2D vs 3D comparison, including OTP, shortly.

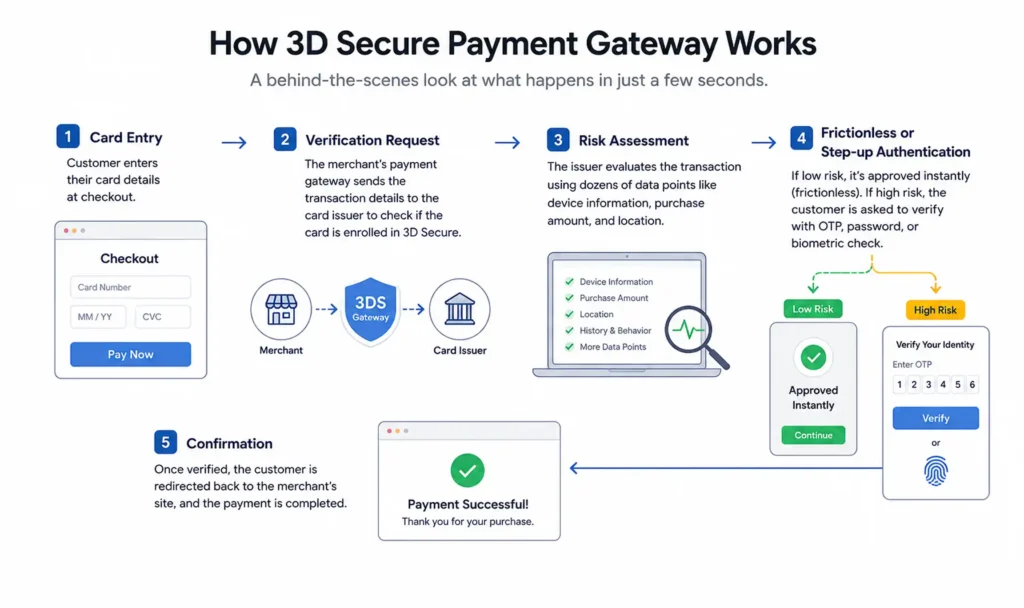

How does a 3D Secure payment gateway work?

Here’s what actually happens behind the scenes during a 3D Secure payment, step by step:

- Card entry: The customer enters their card details at checkout.

- Verification request: The merchant’s payment gateway sends the transaction details to the card issuer to check if the card is enrolled in 3D Secure.

- Risk assessment: The issuer evaluates the transaction using dozens of data points like device information, purchase amount, and location.

- Frictionless or step-up authentication: If the transaction looks low risk, it’s approved instantly with no extra input from the customer. If it looks like a higher risk, the customer is asked to verify with an OTP, password, or biometric check.

- Confirmation: Once verified, the customer is redirected back to the merchant’s site, and the payment is completed.

This entire process usually takes just a few seconds. It’s a much smarter system than the old static-password version, and it’s a big part of why explaining 3D Secure payment protocols matters if you’re choosing a gateway for a high-risk or high-ticket business.

If your customers are also entering card details manually rather than through a wallet, it helps to be transparent about how that data is protected.

Our credit card fraud guide covers the risks a 3D payment gateway is specifically designed to reduce.

3D Secure 1.0 vs 3D Secure 2.0

The original version of 3D Secure launched in the early 2000s and worked, but it wasn’t exactly loved by customers. It relied on static passwords and redirected shoppers to a separate authentication page, which often felt clunky and increased cart abandonment.

3D Secure 2.0 (3DS2) fixed most of that. 3DS2 can reduce checkout time by up to 85% and lower cart abandonment rates by as much as 70% compared to the original version, largely because most transactions are now approved frictionlessly in the background.

A few things changed with 3DS2:

- More data, better decisions: 3D Secure 2.0 analyzes over 100 data points per transaction instead of relying on a password alone.

- Mobile-first design: It supports in-app authentication through SDKs, not just browser redirects.

- Biometric support: Fingerprint and face recognition are now valid authentication methods.

- Wider device support: Wearables and digital wallets are supported, not just desktop browsers.

This shift happened largely because of the EU’s Revised Payment Services Directive (PSD2), which required Strong Customer Authentication (SCA) for online payments.

As Stripe notes, adoption of 3DS2 picked up significantly around 2019 as businesses worked to meet these new regulatory requirements.

Subscribe Newsletter

Subscribe to our newsletter for updates, exclusive offers, and news you won’t miss!

Benefits of a 3D Secure payment gateway

A well-implemented 3D Secure payment gateway does more than block fraud. Here’s what it actually brings to your business and to the people buying from you.

For you as a small business owner:

- Stronger fraud prevention: Verifying the cardholder’s identity before approval makes it much harder for stolen card details to be used successfully against your store.

- Liability shift: When a transaction is properly authenticated through 3D Secure and later disputed as fraudulent, liability generally shifts from the merchant to the card issuer, which can meaningfully cut down chargeback losses, money you’d otherwise lose along with the product

- Higher authorization rates: Visa reports a 9% lift in authorization approval rates for transactions authenticated through Visa Secure, which means fewer legitimate sales get declined by mistake.

- Regulatory compliance without extra paperwork: If you serve customers in the EU or UK, 3D Secure payment protocols help you meet PSD2’s Strong Customer Authentication requirements automatically, so you’re not scrambling to stay compliant later.

- Fewer disputes to manage manually: As a solo founder or small team, you probably don’t have a dedicated fraud or disputes department. 3D Secure quietly reduces how often you need to deal with chargebacks in the first place.

- Easier to work with your bank and processor: Fewer fraud incidents and chargebacks make it easier to maintain a healthy merchant account, which matters a lot if you’re a smaller or newer business without years of processing history.

For your customers:

- Peace of mind entering card details: Seeing a recognizable verification step, especially one tied to their own bank, reassures customers that their card isn’t just floating around unprotected.

- Protection if their card is ever compromised elsewhere: Since 3D Secure confirms it’s really them at the point of payment, it becomes much harder for someone else to use their stolen card on your store, even if the details leaked somewhere unrelated.

- Faster resolution if something does go wrong: Because the issuing bank is involved in verifying the transaction, customers dealing with a fraudulent charge often have an easier, faster dispute process with their bank.

- A smoother experience than they expect: With 3D Secure 2.0, most genuine customers won’t even notice the extra step, since low-risk transactions are approved frictionlessly in the background.

Online Payment Security Handbook

A SAFETY CHECKLIST TO PROTECT YOUR ONLINE PAYMENT

A single security breach can be devastating. This e-book outlines the essential practices that businesses should apply to safeguard online transactions and build a trusted environment.

3D Secure vs 2D payment gateway

3D secure payment gateways prioritize security, 2D payment gateways prioritize speed. The table below breaks down exactly where they differ, so you can pick what actually fits your business

| Feature | 2D payment gateway | 3D Secure payment gateway |

|---|---|---|

| Authentication | Card number, expiry date, and CVV only | Card details plus identity verification (OTP, biometric, or risk-based check) |

| Checkout speed | Fastest, no extra step | Slightly slower for step-up cases, near-instant for frictionless flows |

| Fraud protection | Lower relies only on card data | Higher, adds real-time identity verification |

| Chargeback liability | Usually stays with the merchant | Often shifts to the card issuer once authenticated |

| Best for | Low-risk, high-volume, fast checkouts | High-risk transactions, international sales, regulated markets |

| Regulatory fit | Not built for PSD2/SCA requirements | Designed to meet PSD2 and similar regulations |

Neither one is strictly “better.” A 2D payment gateway makes sense if you’re optimizing purely for speed and your risk profile is low.

A 3D Secure payment gateway makes more sense if you’re dealing with higher transaction values, international customers, or regulatory requirements.

Many businesses actually use both, defaulting to 2D for low-risk domestic transactions and triggering 3D Secure automatically for anything flagged as higher risk.

Related read: 2D Payment Gateway: Transactions Without OTP

3D payment gateway sites list

If you’re looking for a list of 3D Secure payment gateway providers, here are the ones worth knowing:

- Stripe: Automatically triggers 3D Secure for transactions that require it under SCA, with strong documentation for developers.

- PayPal: It supports 3D Secure authentication for card transactions processed through its advanced checkout, in addition to its standard wallet payments.

- Braintree: It offers 3D Secure 2.0 as a built-in option, popular for mobile-first businesses.

- Authorize.Net: Being a popular 2D payment gateway in the USA, Authorize.Net supports 3D payments too. It gives you the flexibility to choose per transaction.

- Adyen: Strong risk-based authentication engine, commonly used by larger international merchants.

- Checkout.com: It was built specifically with SCA and PSD2 compliance in mind for EU-facing businesses.

- Mollie: Mollie supports 3DS payment across all major card payments and local European payment methods.

- RazorPay: India’s most widely used gateway, supports 3D Secure OTP authentication alongside UPI, net banking, and wallet payments.

- Flutterwave: A gateway built for African markets supports 3DS credit card payment verification across multiple currencies and countries.

- Xendit: a leading gateway across Southeast Asia, with 3DS payment support for card payments in Indonesia, the Philippines, and beyond.

- Wise: Primarily known for multi-currency transfers, it also supports secure card verification for business payments across borders.

- Nuvei: It offers smart 3DS routing and exemption management to reduce unnecessary friction for low-risk transactions.

- PayU: Widely used across emerging markets like India and Latin America, with mandatory 3D Secure flows built in.

The good news is you don’t need to evaluate all of these on your own. Paymattic already supports most of these 3D secure payment gateways out of the box, and setting any of them up takes just a few minutes with no coding involved.

How to integrate a 3D Secure payment gateway in WordPress

Among all the 3D payment gateway sites we’ve listed above, Paymattic supports Stripe (Free), PayPal, Authorize.net, Mollie, Razorpay, Xendit, and Flutterwave with a seamless integration.

If you’re running a WordPress site, let’s see how you can integrate a 3D payment gateway (e.g., Stripe) in Paymattic and accept card payments.

Download the free Paymattic plugin here 👇

Here’s how to set it up:

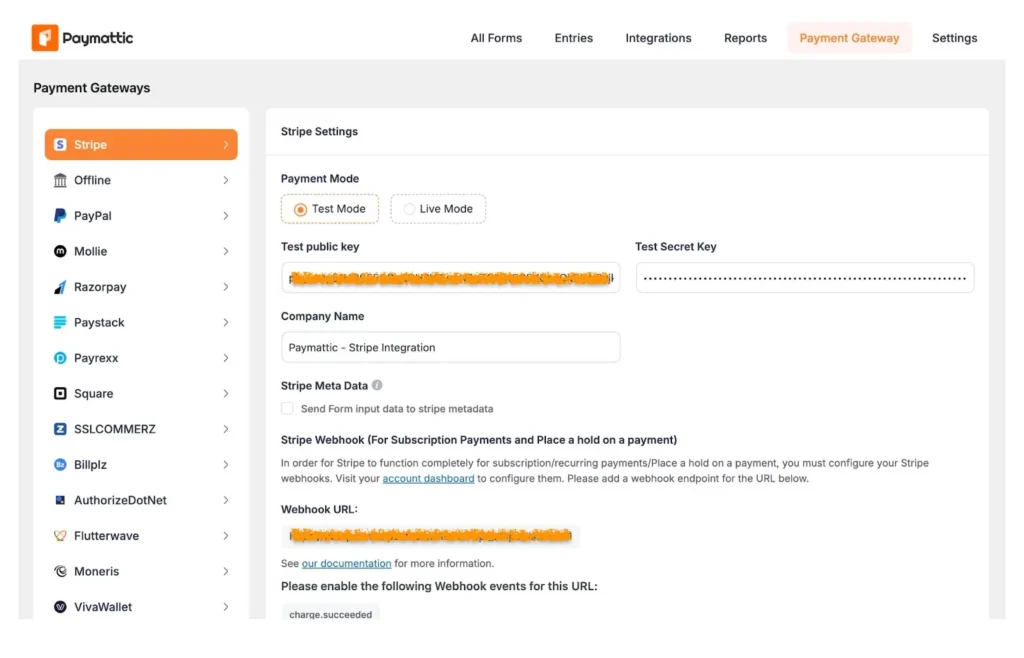

- Install the Paymattic plugin on your WordPress site

- Go to Paymattic > Payment Gateway

You’ll see a list of 2D and 3D payment gateways here.

- Choose a gateway like Stripe

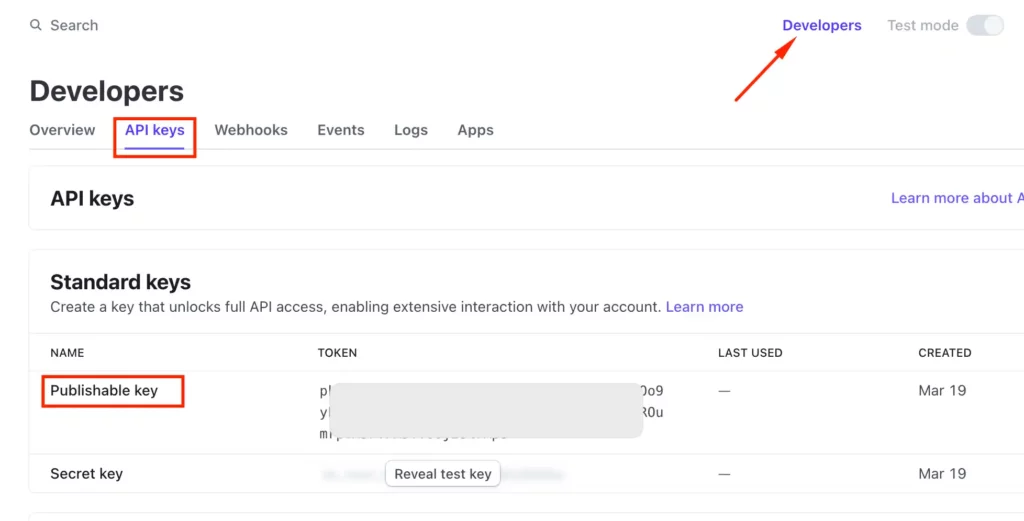

You’ll need the API credentials here.

- Log in to your Stripe dashboard

- Go to Developers > API keys, and grab your Publishable key and Secret key (if you’re not sure where to find these, our Stripe API keys guide covers it step by step)

- Paste the keys into the matching fields in Paymattic

- Click Save Settings

That’s all you need to configure a 3D Secure payment gateway on your WordPress website with Paymattic. Follow the same procedure to integrate any other 3D payment methods.

Once connected, Stripe automatically handles 3D Secure authentication for transactions that require it, whether that’s because of SCA regulations or your own risk settings.

You don’t need to build any of the verification flow yourself.

Before going live with any of the payment methods, it’s worth running test transactions first.

Our guides on Stripe test card numbers and PayPal test card numbers will help you simulate both successful and declined 3D Secure flows without touching real money.

Still unsure about the integration? Watch this video:

Wrapping up

A 3D Secure payment gateway isn’t just a compliance checkbox. It’s a real tool for cutting fraud, protecting your chargeback rate, and building enough trust that customers actually finish their purchase instead of abandoning the cart at the last second.

If speed is your only priority and your risk is genuinely low, a 2D payment gateway might still make sense.

But for most businesses handling card-not-present transactions, especially at higher values or across borders, 3DS payments are worth the small amount of extra friction.

Setting it up on WordPress takes a few minutes with Paymattic. Give it a try and see how it affects your authorization rates.

Join the thousands already enjoying Paymattic Pro!

Tipu Deb

Hey! Tipu here, working as a Marketing Strategist at WPManageNinja & Paymattic. A nature lover and a person who is addicted to exploring historical events. In my leisure, you’ll find me playing with different musical instruments.

Leave a Reply